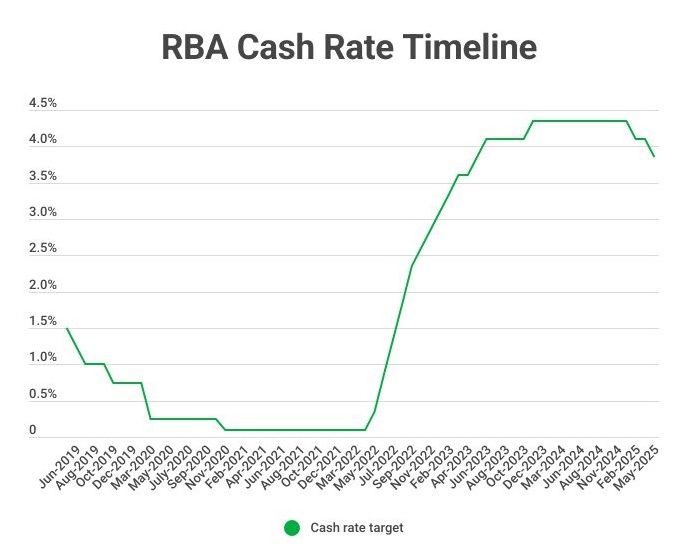

Australia’s mortgage holders and property buyers have received welcome news: the Reserve Bank of Australia (RBA) has cut the official cash rate by 0.25%, bringing it down to 3.85% as of May 2025. This is the second rate cut this year, and it marks a significant moment for the housing and lending market, offering some relief after a period of higher interest rates and cost-of-living pressures.

Why Did the RBA Cut the Cash Rate?

The RBA’s decision was driven mainly by easing inflation and a slowing economy. Recent data shows that inflation has now returned to the RBA’s target band of 2–3%. The Consumer Price Index (CPI) rose just 2.4% over the past year, and the RBA’s preferred measure of core inflation (the trimmed mean) fell to 2.9%—its lowest in over three years. This return to target inflation gave the RBA the confidence to ease monetary policy. Economists also pointed to slower economic growth and cautious consumer spending. Annual GDP growth has slowed to 1.3%, and retail turnover has been flat in early 2025, indicating that households are still feeling the pinch and spending less. While the job market remains resilient, with unemployment steady at 4.1%, there are signs that the economy is losing momentum. The RBA noted, “The risks to inflation have become more balanced. Inflation is in the target band and upside risks appear to have diminished as international developments are expected to weigh on the economy… The Board therefore judged that an easing in monetary policy at this meeting was appropriate”.What Does This Mean for Your Mortgage?

For homeowners with a variable-rate mortgage, a 0.25% rate cut could translate into real savings. On an average home loan of $659,920, this cut could reduce repayments by about $106 a month, or $1,272 a year. Combined with the earlier cut this year, the total annual saving could be $2,553—assuming your lender passes on the full reduction. If you have a $500,000 loan, you might see your monthly repayments fall by around $80, or $960 a year. For those with larger loans, the savings add up even more. But not all banks automatically pass on the full cut. Some lenders may only reduce rates partially, or delay the change. It’s important to check with your lender and compare your rate to what’s available in the market. If your lender isn’t offering the full benefit, you have the right to refinance or switch to a lender with better rates.What About New Borrowers and First Home Buyers?

Lower interest rates mean increased borrowing power for new buyers. With the cash rate now at its lowest in two years, lenders are competing for new customers, and some are already offering variable rates below 6%—with more than 30 lenders expected to have at least one rate under 5.5%. This competition can help first home buyers and those looking to upgrade or invest, as borrowing costs fall and more attractive deals become available. Mortgage brokers are seeing renewed interest from buyers and refinancers. The rate cut cycle is expected to energize the property market, with more people able to qualify for loans and more homeowners considering refinancing to secure a better deal.

Should You Lower Your Repayments or Keep Them the Same?

While lower interest rates mean you can reduce your monthly mortgage repayments, many experts recommend keeping your repayments at the same level if you can afford it. By doing so, you’ll pay off your loan faster and save even more on interest over the life of your mortgage. For example, if you have a $600,000 loan and maintain your previous repayment amount after a rate cut, you could save up to $89,000 in interest and pay off your mortgage four years earlier. This strategy builds a financial buffer and gives you more flexibility in the future.What Should You Do Next?

- Check if your lender is passing on the full rate cut. Not all banks do this automatically, so contact your lender or mortgage broker to confirm your new rate.

- Compare your rate to the market. With increased competition, now is a good time to shop around. Many lenders are offering special deals for new customers and refinancers.

- Consider refinancing. If your lender isn’t competitive, refinancing could save you thousands over the life of your loan.

- Review your repayment strategy. If you can, keep your repayments at the previous higher level to pay off your mortgage faster and save on interest.